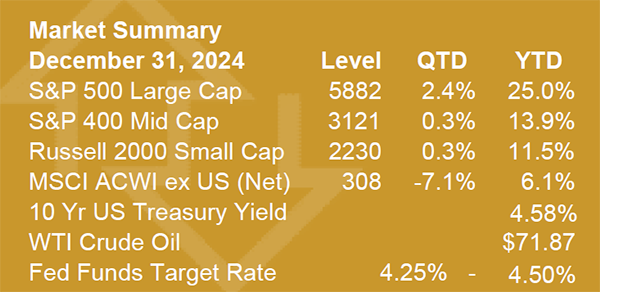

Summary

In the last quarter of the year, the economy and markets showed continued resiliency on the strength of consumers and the expectation that the election, which resulted in Republican control of all three branches of the U.S. government, will likely lead to lower regulation and continued low tax rates. However, inflation also continued to prove resilient, despite the Federal Reserve (Fed) beginning its rate cutting cycle at the end of the third quarter. In light of the Fed lowering short term rates and economic growth being durable, the yield curve steepened across maturities longer than one year, indicating lower expectations of a recession.

U.S. Large Cap Growth stocks continued to lead the market forward, with a brief but short-lived surge following the U.S. national election. U.S. equities had a strong showing over the full quarter.

The Economy

U.S. Real Gross Domestic Product (GDP) growth expectations have risen from just under 1% quarter-over-quarter to a robust 2% as consumers continued to spend. Besides solid retail sales in October and November, Black Friday and Cyber Monday sales reportedly reached record highs. Consumers were buoyed by the lowest gas prices of the year and few signs of mass layoffs, despite new jobs opening data continuing to slow. While the Initial Jobless Claims 4-week moving average has remained below 240,000 for the entire quarter, Continuing Jobless Claims have reached their highest level since 2021, albeit a modest 5% move upwards since the beginning of the year. Manufacturing, however, has continued to contract as the ISM Manufacturing PMI indicator has remained under 50 since April but has improved over the quarter.

Prices swung away from the Fed’s 2% target as both the Personal Consumption Expenditures Index (PCE) and the Consumer Price Index (CPI) showed increases that were larger than the year’s low mark in September. Both measurements, however, were low enough so as to not deter the Fed from continuing to cut rates at both of its fourth quarter meetings.

However, while the lower Fed Funds rate helped short-term borrowers, longer term borrowers, such as those seeking mortgages, saw long-term rates rise in the quarter with the Freddie Mac Primary Mortgage Market Survey showing an 11.5% rise to 6.85% in the 30-year fixed mortgage rate and a 16% rise to 6.00% in the 15-year fixed mortgage rate over the quarter. Despite the rise in rates, the real estate market showed a strong improvement in activity as more sellers emerged and buyers either eschewed financing or decided they couldn’t wait any longer. To close the year, pending home sales data notched its first positive four-month run since 2020 and building permit issuance increased. We note that this run began in the same month as the first Fed rate cut.

Globally, most major economies continue to struggle with growth but have seen success against inflation. The continued strength of the dollar and potential U.S. trade policies in 2025 have raised concerns among global policymakers and investors, pressuring both developed and emerging market equities.

Markets

U.S. equities had a good quarter, capping the best two years of equity returns since 1997-1998. Following the trend of the year, U.S. large cap growth led the way, with the Russell 1000 Growth Index outperforming the Russell 1000 Value Index, 7% vs -2%, for the quarter. Also consistent with the trends of the year, the positive return was largely carried by the Magnificent 7, 16% vs the S&P 500’s 2.4%. Mid- and small-cap stocks were flat for the quarter. The Consumer Discretionary sector led the way over the quarter, returning nearly 14% with the Telecommunications Services (9%) and Financial (7%) sectors returning positive returns. The Materials (-13%) and Healthcare (-10%) sectors were the weakest. For the year, the Telecommunications Services (39%) and Information Technology (36%) sectors led the way while the Materials (-1.8%) and Healthcare (+0.9%) sectors were the weakest. For the year, the Russell 1000 Growth Index outperformed the Russell 1000 Value Index, 33% to 14%, respectively.

For 4Q24, the estimated year-over-year earnings growth rate for the S&P 500 is expected to be 14.6%. This would be the highest growth rate in the index since 2021. While earnings growth is expected to be strong, the results of the U.S. election raised expectations for a stable or lower tax regime and less regulation, particularly for the financial sector.

However, global trade policy has raised questions for specific industries, such as agriculture and manufacturing. The S&P 500 forward Price/Earnings (PE) Ratio ended the year at 21.6x.

In another sign of the strength of the economy, corporate yield spreads narrowed to their tightest level since 1995. Meanwhile, the benchmark ten-year U.S. Treasury Note rose from 3.75% to 4.6% over the quarter as investors worried that inflation was rearing its head once again.

Looking Forward

We enter 2025 with a growing economy despite continued contraction in the manufacturing sector. Inflation remains sticky enough that the expected number of rate cuts in 2025 continues to fall. The Fed itself has projected just two 25 basis point rate cuts by the end of the new year. This could result in higher longer-term rates lingering longer than previously expected; though a steepening normal yield curve would be favored by many financial institutions as a sign of stability. While higher rates may put a damper on risk asset returns or create volatility in the equity markets in light of current valuations, it could be a sign that the risk to the economy has eased, and a soft landing has a good probability. We can expect efforts to weaken the U.S. dollar, both from foreign policymakers and our own, in order to lower costs for foreign consumers and promote U.S. manufacturing. While tariffs run counter to this goal in theory, the actual application of tariffs remains to be seen. A softer dollar with selectively targeted tariffs would be good for U.S. manufacturing but it will require a delicate balance and deliberate negotiations.

As the last two years have been the strongest two-year period since 1997-1998 for U.S. Large Cap equities, valuations are elevated versus historical averages and interest rates will likely remain near current levels. We also expect some volatility in risk assets in the coming year. However, there is still upside in equities if the economy and consumers remain resilient, U.S. manufacturing recovers and corporate earnings continue to grow consistently. Meanwhile, fixed income does offer reasonable yields for the capital preservation/income side of investment portfolios, particularly in safer credits as yield spreads finished the year at its tightest level since 1995. In addition, if the Fed quickly achieves its target level of rates with just two or fewer cuts, cash reserves could enjoy only a modest decrease in yield this year.

Sandy Spring Trust provides true, trusted and transparent strategies to protect your family and support your businesses and manage your assets. Call 800.877.5417.